Archive

The Business of Fashion – Regulation, acquisition and the slowdown

When the global financial meltdown struck in 2008, many of those with a vested interest in the luxury market watched nervously; high net worth individuals had surely seen many investments wiped out as the recession struck and would thus be more inclined to austerity. While there was a brief moment of humility and caution over indulgence in life’s finer things, it was brief. The luxury market proved surprisingly resilient. Global spend has increased since the recession by around a third, helped in no small part by the explosion of growth in developing regions, China in particular. Orson Welles once said “If you want a happy ending, that depends of course on where you end your story”. Our story, sadly, does not end here.

It was not a good omen when fashion curator and director of the Musée Galliera in Paris Olivier Saillard said during New York Fashion Week last month, “We are in a moment that’s very bizarre in fashion: there are too many clothes”. Business of Fashion lamented both a lack of quality and vision in contemporary collections,

“Fashion seems stuck between the need to surprise using a new array of communications tools and the urge to deliver novelty at the fastest possible pace. Slowing down might be a solution, but that would be a hard route, which will hardly find followers.”

And it is followers that fashion, and the luxury market as a whole, are in need of. Earlier this month the Financial Times reported on the global slowdown of luxury spending. Behind this slowdown lie two factors. On the one hand, there is what are hopefully short-term influences; geopolitical turmoil is rife. Hong Kong continues to see protests that refuse to simmer down, causing disruption to myriad businesses. The city accounts for perhaps 20% of global luxury spending. The Middle East, whose consumer origin or nationality according to Bain & Co. has the biggest average per capita spend, is similarly in chaos, with Syria, Iraq, Afghanistan, Egypt, Libya all in various stages of unrest. Regions like Saudi Arabia and Qatar are caught between a rock and a hard place. In Russia, sanctions have hit oligarchs and their ilk hard. As a result, shares in luxury good companies have been hit hard. Prada has seen profits slide 20% in the first half of the year. Everyone’s darling of fashion innovation, Burberry, has warned of a “cautious outlook”. Mulberry has issued a string of profit warnings and recently ejected its CEO.

McKinsey illustrate the drift of luxury growth from developed to emerging markets

So we can reason that these companies are seeing fewer customers. But they are also attracting new ones, albeit with very different expectations of the service they expect from the companies they have relationships with. This is the longer-term challenge. Millennials may have been treated as a distinct niche group with quirky demands from brands, but next year they will outnumber Gen Xers, according to McKinsey. These utterly digitally savvy citizens have embraced and contributed to a digital fragmentation in the consumer decision journey, the production process and the fundamental nature of buyer / seller value exchange.

“[A] confluence of digital, the rising power of street fashion and changing consumer attitudes… are radically altering the industry. [It is a] consumer-led shift away from ostentatious and mainstream mega-brands towards understated originality”

One of the most obvious ramifications of this has been the trend of ‘logo fatigue’. It is likely to hit those like Gucci particularly hard, while benefiting those like The Row, and little-known retailers like L’Art du Basic. For larger brands there are some examples for inspiration though. Yoox, whom we have profiled in detail before, have gone from strength to strength in embracing effective digital strategy. The fashion ecommerce site reportedly sees 42% of its global traffic coming from mobile devices, and has recently made a significant push into experimenting with instant messaging app WeChat. As elaborated by Fashion and Mash, the account allows users to “shop via an interactive look book, and to instant message customer service teams and personal stylists. Content also invites users to exclusive events and provides early access to specific products”. In the physical world, Ralph Lauren’s hosting of a cafe in its Fifth Avenue store in New York may be less immediately strategic but seeks to leverage the same burgeoning trends. Brands will need to do more of this, more often, if they are to find what works best for them in terms of engaging and converting future prospects.

Also this month, Zeitgeist found itself at an event at London’s Four Seasons hotel off Park Lane, hosted by law firm Baker & McKenzie. Threats, tech trends and M&A were the main subjects of discussion. Zeitgeist scribbled down some bons mots which were thought worth recounting here. Last month, McKinsey produced an insightful piece on the future of luxury growth, indicating growth would come for the most part from what they termed global megacities, a large proportion of which were located in emerging economies. But China is facing a slowdown; no doubt one of the reasons it was recommended in the conference that businesses start to think less of China as an independent market of growth and more of ASEAN as a region.

3D printing was a matter of much conjecture, but it was pleasing to see that the regulation of such materials was already being considered. One speaker offered the technology would be a greater problem for toy manufacturers than luxury, but cautioned that fast fashion and high customisation were a potent mix. Current UK regulation allows for printing any designs (of one’s own creation or not) at home for personal use for no gain. Such laws may have to be re-examined as 3D printing becomes more widespread. It is difficult to protect the IP of a fashion designer’s work, and difficult therefore to know where to draw the line between inspiration and infringement. The case of the red shoe, specifically between Yves Saint Laurent and Christian Louboutin, has illustrated such difficulty. In the case of 3D printing, one speaker suggested that printing could be limited via restriction similar to how publishers use paywalls, or a more sophisticated version of the DCMA. The importance of protecting the source code of 3D printing designs looks set to be important; Pirate Bay already has a section for such product. Social networking as a new source of IP was also discussed. David Yurman sought opinions on styles to be included on a Valentine’s campaign; users could drop hints to their partner. Bergdorf encouraged fans to design Fendi bags over social, too. But there have been slip ups; Cole Haan offered to pay fans $1,000 for taking pictures of their shoes, without making it clear it was part of contest where someone would win and that the company was sponsoring the activity. They got off with a warning from the regulator, but luxury brands must treat that as a cautionary tale as they continue to experiment. “The law is not keeping up with the technology”, as one speaker sagely confessed.

David Yurman’s Facebook campaign suggests new IP possibilities for businesses in the future

The M&A chat was equally of interest. Speakers ruminated on the rise of vertical integration as LVMH et al seek to own the whole process. It’s a brave step for companies that traditionally haven’t involved themselves with supply chains or distribution, according to those speaking. Acquisitions were taking two forms: one was spotting missing gaps in the portfolio. For LVMH, the hole in their portfolio was jewellery, which lay behind their purchase of Bulgari in 2011. More recently Giorgio Armani – or as one speaker referred to the man himself, “King George” – reclaimed control of Armani Exchange as it attempts to leverage fast fashion trends. The other form was that of acquisitions in support of brand development – innovation, technology, CRM in Mandarin, social media, etc. More of these sorts of acquisitions were expected on the horizon.

How do these deals play out today? Private equity buyers have a lot of capital and access to cheap debt, but traditionally many of the targets of a buyout have been family-owned businesses who were not ready to relinquish control to a PE firm. These firms are much quicker and more aggressive at deals; they can quickly globalise a brand, can improve the supply chain and stretch the brand up and down from the original price point. Of course, adding new assets, like social media, makes due diligence – and knowing how to allocate risk to a mercurial medium – much harder. Owning supply chains carries risks of more exposure (see Apple and Foxconn). One of the most thorny issues that speakers envisioned was for a luxury good empire known for provenance and quality to be acquired by a a company in a jursidiction that is not known for such things. What if Alibaba bought Balenciaga from Kering, for example?

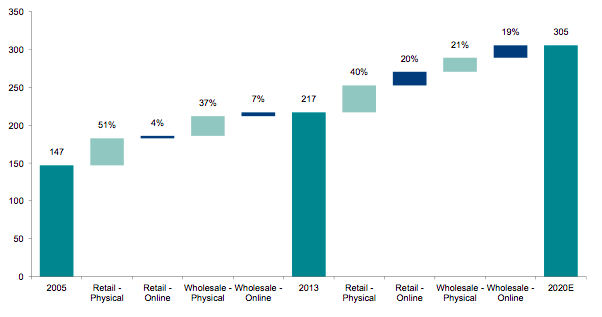

Digital is expected to drive, on average, 40% of projected luxury sales growth from 2013 to 2020

Next year will see the return of John Galliano to the runway stage to the helm of a fashion house, this time at Martin Margiela. A recent article on the designer’s flameout while creating works of wonder for Christian Dior emphasised the way in which Galliano “had been cloistered off into a strange protective bubble. Sometimes, we isolate (and elevate) talented creatives so much in the fashion industry that they lose connection with reality”. It is arguably a similarly protective bubble that the fashion industry itself has often been accused of being in, and we would argue it is in now with regards to the need for greater digital sophistication and a more significant investment in digital strategy as it concerns customer insights and the law. It is plain to see that the luxury industry continues to face disruptive challenges, be they at the hands of digital, demographic or geopolitical trends. Some of these disruptions will hopefully, as mentioned earlier, be more temporary in nature. The more fundamental shifts in consumption, though challenging, also present myriad opportunities for businesses that are brave and agile enough to test what works best to capture and retain the customer of the future. Last month Exane BNP Paribas published a report illustrating just how important digital sophistication will be (see above chart), and naming those most likely to benefit from such changes. They could do worse than start by reading our previous post on the future of retail.

Luxury still too good for a digital strategy

Chanel is one of the key culprits when it comes to lack of digital innovation

A recent McKinsey report declared that, for businesses, “The age of experimentation with digital is over“. That may be for most B2B and B2C private sector companies, but not for the luxury goods industry. Bemoaning the woeful development and investment in strategic initiatives for luxury brands online is something this blog has done once or twice before. There are understandable reasons why the industry has been reticent to commit to online retail, based on customer insight (the assumption that HNWIs don’t like to shop for something without being able to see and touch it for themselves) and conflicting priorities (physical store expansion into China and more experiential events has been the name of the game in recent years). But with a China slowdown mooted, particularly in the area of luxury gifting, and no real concrete research to show that HNWIs aren’t just as digitally savvy as their less liquid counterparts, there becomes less and less justification for what are, across the industry, woeful examples of digital strategy and innovation.

It can’t be easy for profitable businesses like LVMH, with an eye on quarterly earnings, to make drastic investments in the online space. Luxury’s brand equity often comes from provenance and tradition; a company’s roots are in its founding stores, the connotations of Milan, Florence, Paris, etc. They also worry about their neighbours; a flash-sale site or, worse, one full of counterfeit knock-offs, is always just a click away. From a logistical point of view, there is also the issue of back-end infrastructure to contend with. For several years, PPR (now Kering) ran much of its e-commerce business through Yoox, as we’ve talked about before. It would be wrong to single out those in luxury. L2 Thinktank recently tweeted with much excitement about Bacardi’s “cocktail discovery site” that worked seamlessly across web, mobile and tablet. Well, forgive us if we don’t leap for joy in an ecstasy of delirium, but this is 2014, that should be the minimum deliverable. Still, luxury is a sector in blatant need of redirection.

eConsultancy eviscerated many luxury brands’ online presences in a recent article

Burberry is lauded by many as an outlier in this world of luxury goods, a company that has truly embraced digital. For all the talk of such innovation though, the website itself is utterly dominated by a rote e-commerce site, as are its social networks such as Google+. It is the physical stores where technological innovation has been injected. And this is supposedly the company pushing the rest of its peers forward. It comes as little surprise then that eConsultancy published a superb piece at the end of April excoriating the sector, leaving no brand unscathed. Headlines included, “painfully slow load times“, “awful UX” and “not making much effort“. But the worst and most perplexing atrocity had to be the above screengrab on the purposeful hiding away of an e-commerce platform, one that was presumably quite expensive to source and implement in the first place. We can’t overestimate the necessity of having a clear user journey through to purchase, just as it would be difficult to overestimate the amount of luxury good companies that are guilty of this sin for which Dolce & Gabbana have been singled out for here.

On this note, Gucci’s recently relaunched mobile site – replacing among other things a tablet site that had been left to wither since 2010 – was welcome news to us, as it seemed to be also (logically) to those wishing to actually part with their money on Gucci wares. L2 in May reported the news, saying that the new site now accounts for 27% of all traffic, a 150% YoY increase. Sounds good, except that means traffic through the mobile site in 2013 was a miniscule 0.18%, right? Terrible.

There are signs of hope. Gucci’s move to invest in a new mobile site, though monumentally belated, is a welcome one. As more brands cotton on to the importance of online, the Financial Times recently reported on the moves many are making to secure ‘.luxury’ suffixes, in the wake of IPv6, if only to avoid the complications of cybersquatting. And Michael Kors, which seems only to be going from strength to strength every quarter, has praised its own social media presence for “driving international sales”. We’ve almost entirely focused on fashion brands here, but other companies within the luxury sector are getting the message loud and clear. Take the auction house Christie’s, a legacy company if ever there was one, having been founded in 1766. Not only have they dedicated time and energy to investing in major online auctions, they have also recently created a new sector vertical of ‘luxury’ within the house itself. New thinking might well take new talent, it will also take C-suite buy-in, as well an acceptance that digital commerce is an integral part of business now, no matter how exclusive your product is.

Taking flight – Opportunities and obstacles in democratising luxury

I don’t think democratic luxury exists. I don’t believe in something for everyone… How can we possibly put these products on the Web site without the tactile experience of luxury?”

– Brunello Cucinelli

The democratisation of fashion took a beating this past week as news reached Zeitgeist that Fashion’s Night Out was to be no more. Spearheaded by Anna Wintour at the height of the global recession, the idea was for a curated evening; a chance for stores to open their doors late, inviting a party atmosphere and focussing spend on a calendar event. The Wall Street Journal wrote that last year, “Michael Kors judged a karaoke competition at his store on Madison Avenue, rapper Azealia Banks performed at the MAC store in Soho and a game night was held at a Kate Spade store.” The evening festivities were replicated across New York, London and other cities.

Zeitgeist happened to be on Manahattan’s Spring Street last September when the most recent FNO was held, waiting patiently for a perenially-late friend who works next door to Mulberry. While waiting, it was absolutely fascinating to see the sheer of variety of people out on the street. While the crowds were mostly composed of women, the groups ranged from college-aged JAPs and the avant-garde to hipsters and stay-at-home mothers. Most gawped excitedly as they beheld the Mulberry boutique, enticed by the glimpses of free food and drink, as well the sultry bass tones of some cool track. One elegantly dressed fashionista strode hurriedly past Zeitgeist, lamenting to her cellphone “Oh God, it’s Fashion’s Night Out tonight”.

Ultimately perhaps it was such feelings among the fashion set that caused FNO to come to an abrupt end. But Zeitgeist got the sense that, while undeniably a celebration of fashion and an opportunity for brands to showcase their attractively experiential side – particularly to those who might usually be deterred by luxury brands and their perceived sense of formality – there weren’t a great deal of people actually buying things. It’s quite possible that the whole strategy of attracting a crowd who would not otherwise frequent such stores backfired; they turned up, sampled the free booze, felt what it must be like to shop at such-and-such a label, then moved on to the next faux-glitzy event with thumping music. This then was a failed attempt to bring luxury to the masses.

On a macro scale, the cause for democratisation is hardly helped by the global financial crisis. Although over four years old, the ramifications and scarring done to the economy are still sorely felt. This is illustrated in the unemployment figures around the world, tumultuous elections and anecdotal tales of hardship. More starkly, they are being backed up by solid quantitative research that proves we as a world are less connected now than we were in 2007. In December last year, The Economist reported on the DHL Global Connectedness Index, which concluded that connections between countries in 2012 were shallower (meaning less of the nation’s economy is internationalised) and narrower (meaning it connects with fewer countries) than before the recession. Meanwhile, just this past week, the McKinsey Global Institute published a report showing financial capital flows between countries were still 60% below their pre-recession high. This kind of business environment hardly fosters egalitarian conduct, and indeed such isolationist thinking was on show at Paris Fashion Week recently, where designers clung to their French heritage as a badge of honour. Exactly at the time when art needs to be leading the way in cultural integration, as emerging markets not only continue to make up a larger part of the customer base, but also develop their own powerful brands, it seemed that designers, like the financial markets, retreated to what they knew and found safe.

The world is less connected today than in 2007

Where the ideology of democratising fashion has seen more success is of course online. We’ve written before about how luxury is struggling with the extent to which they invest in e-commerce. One of the principle hurdles is that the nature of luxury – elite, arcane, exclusive – is more or less diametrically opposed to the nature of the Internet – open, borderless, democratic.

Yet the story of Yoox – the popular and, in online terms, long-lasting fashion ecommerce platform – and its founder is one of just such democratisation. (It is particularly stunning to read of the difficulties the founder, a Columbia MBA graduate, Lehman Brothers and Bain & Co. alum, had in attracting VC funding). It also, crucially, points to the importance of recognizing multiple audiences, and how they like to shop differently depending on context. John Seabrook, writing in The New Yorker, reports that when Federico Marchetti set up Yoox in 2000, the world of ecommerce for fashion was regarded as a not particularly salubrious environment. Rather, the magazine compares it to outlet stores like Woodbury Common, fifty miles north of New York. Luxury brands like Prada and Marni could be found there, offering deep discounts on their wares, and it was for that reason – and the lack of control over their own brand – that they didn’t like much to talk about such places. This, despite the fact that they attracted 12 million people in 2011, “almost twice the number of visitors to the Metropolitan Museum”. Yoox was likewise greeted with much trepidation by fashion retailers. The article quotes an analyst from Forrester Research:

“It was a matter of principle with luxury brands that only people who shop on eBay use the internet – and their only interest was in getting a low price.”

Marchetti’s only available source of designer clothing was from last season and beyond, as no brand would sell their current collection. He curried favour with some of them though by advertising the prices without noting the discount customers were getting. Other than that, luxury brands took little or no notice.

Online shopping though would prove to be “one of the largest disruptions of the luxury-goods industry since the birth of the department store”. There are three kinds of online store today; those that sell deep-discounted goods on end-of-season wear, those that sell in-season clothing, and those that have flash sales of small numbers of clothing or accessories. It turned out there was an audience for all of these types of website. Bridget Foley, executive editor of WWD is quoted in the article saying “[T]here has been a sea change in attitude… I think [it] surprised the fashion industry… Just because you love clothes doesn’t mean you love shopping“. This struck Zeitgeist as one of the more important insights in the lengthy article. Though retailers often harp on about the importance of the retail environment, the need to touch the product, to be in an atmosphere where everything has been curated down to the finest detail, online neutralises all of that. This idea threatens those in the luxury sector, as the thinking goes that any such premium on products may seem less justifiable away from a Peter Marino-designed armchair and a nice glass of champagne. Such ideas are being challenged though. Not only is the nature of the store changing – from robotic sales staff to customers as models on the catwalk – but so is the view of the luxury customer as a homogenous, static group, devoid of context. Zeitgeist was at a Future of Media summit at the Broadcast Video Expo last week, where, as behavioural economics suggest, MD of Commercial, Online and Interactive for ITV Fru Hazlitt insisted that consumers had to be targeted in ways that were pertinent to them, not only as demographic groups, but in ways that recognised the context of how approachable they were likely to be at the time, given the programming they were watching. Fru admitted that in years past, broadcasters like ITV had seen advertising as “space to rent out”. Now they were thinking deeply about how and when is the right moment to reach their target consumer. It is the same in fashion. There is not one single way to reach the consumer; buyers of luxury goods do not want to be solely restricted to being able to buy your wares in a physical store.

Chanel are one of the few remaining luxury brands to resist fully integrating online

Behavioural economics played a role in Marchetti’s initial framing of the audience for the website as well. He hired pedigreed fashion writers, as well as artists, architects and designers to make special projects that lent the website an air of curation, of something more special and rarefied that what one might find – or more importantly the way one might feel – at an outlet mall. Marchetti wanted the customers “to see themselves as connoisseurs, even if they were really just hunting for bargains”. The New Yorker article goes into some anecdotal detail about the way people shop on Yoox, which crucially differs not only from the way they would shop in-store, but also from other e-tailers. For online shopping in general, the experience is one where you can purchase ten items, and return nine of them with very little hassle, with credit for multiple rather than a single brand, and certainly no raised eyebrow from a pretentious shop assistant. Regarding specific sites, Yoox, unlike Net a Porter, for example, does not try to force a set of looks onto the user. Behavioural economics tell us that people irrationally value something more when they’ve been made to work a bit to get it. Such is the case now shopping for luxury items, which makes clothing not in-season (i.e. not currently in every shop window), both cooler and cheaper. It’s an act not to be discouraged. A Saks representative says customers who shop online as well as in store buy four times as much merchandise as customers who shop only in the store. What will worry retailers though is that the convenience of the online store outweighs the experience of the physical boutique. The New Yorker quotes a shopper: “I’ll never buy a dress at the Prada boutique again after getting these really amazing ones on Yoox.”

As well as setting up the Yoox website, Marchetti’s company now also powers the online stores of more than thirty fashion houses, including Armani and Jil Sander. Last summer, PPR joined in too, after conceding that their in-house expertise was not up to snuff. The latest development is making designs available to any customer as soon as it hits the runway. Burberry, as well as separate sites like Moda Operandi, have spearheaded this innovative change, which is effecting editorial as well as buying methods previously seen as unshakeable. The demand for this type of instant purchasing seems to be fueled by a niche – albeit a sizable one – that is not representative of the majority of luxury shoppers. The accessibility of a brand and its products is a tricky one to tread, one which Zeitgeist has written about several times before. Tom Ford performed a volte-face this year, after debuting his womenswear collection with no press and VIPs only, relented this year at London Fashion Week by letting bloggers write about the show. Chanel still steadfastly refuses to fully engage with online shopping. The tension is keenly felt in the New Yorker article, where Amazon’s new entry into the world of fashion is referenced. The CEO of Valentino is unconvinced: “Valentino is high luxury… People going to Amazon are not going to Valentino“. This smacks a little of pride and ignorance, for they most assuredly are, though perhaps not with luxury purchases in mind… yet.

It comes back to the idea that there are myriad types of luxury consumer. The industry has not fully acknowledged as of yet that the buying behaviour of a descendant of the ancien regime in Paris is unlikely to buy in the same way as a newly-minted businessman in Shenzhen. They may know that these types of buyers exist, and they may even create different products for each. Importantly though, they are not recognising that these people may go about purchasing in a different way. It’s not just a purchase journey that has changed massively in recent years, as McKinsey’s consumer decision journey illustrates above. It’s also, as ITV’s Fru Hazlitt insists, about recognising that different people shop in different ways, wholly dependent on context. Though Fashion’s Night Out may be on permanent hiatus, and though the global economy may be sputtering along in second gear, the opportunities to leverage deep insights into consumer purchase preferences are there for the taking. Yoox, along with a deeply complicated algorithm, are trying to tap into just this. But the process must start with realising that yes, actually, someone might want to pick up that Valentino dress while surfing on Amazon.

For Luxury, what price service?

Whither the sage of a shop assistant? At a time when we as consumers have access to all the information we could want about a brand and its products via our smartphones, of what use is it to have someone tell me something that I am unlikely to take at face value, working as they are for said brand? Why even bother being in the store at all when I can be buying my item at home? The luxury goods company PPR (owners of Gucci, Saint Laurent Paris, Balenciaga et al.) could be said to have recently adopted a similar mindset. A new joint venture with e-tailer Yoox is sure to shake things up. Honcho Francois-Henri Pinault said recently, “While the whole industry has been resisting e-commerce for the last 15 years it’s now realising it’s inescapable”.

Not everyone believes such a move is inevitable. Chanel is steadfastly refusing to sell its principle collections – from ready to wear to handbags – online for the foreseeable future, according to a recent interview with the CEO. While this might strike some as akin to sticking one’s head in the sand, the reasoning the company gives centres around the unique experience of going into a store to buy a product, rather than sitting at home in one’s pajamas. From a strategic point of view, the idea is sound. Reducing avenues of purchase encourages a scarcity factor that high-end fashion must rely on. It also ensures that the products are seen in the best light possible, incredibly important when justifying such a premium. It’s interesting to note that though the thinking may be sound, it is certainly not appropriate for every luxury brand to be resisting the lures of online shopping in such a dramatic way. Chanel is – and always will be, in multiple ways – a very special company, an exceptional brand, in the literal sense. Like Apple though, it’s practices are to be emulated with caution, as a great paper by McKinsey Quarterly highlights. “Outliers are exactly that…”, the report states.

But what is the state of stores, and how important is service in these places? For luxury, we can assume a high priority of the physical shopping experience is connected to the person assisting you. Recent experiences at two different luxury goods stores highlighted jarring differences, monumentally affecting the way Zetigeist felt about the brand. Last month in New York, Zeitgeist visited Tiffany & Co. to find a Christening present. Without turning this article into a rambling letter of complaint, the section Zeitgeist found itself in was woefully understaffed, and when help was available, information turned out to be incorrect and, most importantly, not dispensed as if it were important to them. Zeitgeist left without buying anything. The experience was deflating enough to mention to the manager en route to leaving the store. Returning at the weekend to try again, the experience had not much improved. The item needed to be engraved. Taking it into one of the London stores upon returning home meant being greeted with the same mediocre level of service. No passion, no interest. This would be perfectly acceptable for somewhere such as Ernest Jones, but Tiffany is a massively, massively powerful brand. For many it is incredibly evocative, and speaks to nostalgia and deep-seated emotions with very personal connections. There is a dream that is Tiffany, that is replicated extremely well in their above-the-line marketing. It is completely absent in its physical embodiment, the store. Cartier, by comparison, manage to present a fantastical vision of their brand, while also maintaining a consistently excellent level of service in-store that brings cohesion to the image it evinces.

Louis Vuitton could not have presented a starker contrast to Tiffany. The brand had one brief flirtation with TV ads about four years ago. While also a powerful brand, it perhaps could not be said to elicit such powerful emotions as Tiffany, purely on the basis that Tiffany purchases might often be assumed to be gifts. Purchasing what is surely one of the cheapest things in the store, Zeitgeist was delighted to be led through the purchase process by an exceedingly-well trained woman, who was happy to go over the minutiae of the purchase, and knew answers to arcane questions when asked. It made the experience extremely pleasurable. Remarkably, the store went a step further, sending Zeitgeist a random act of kindness and imploring to get in touch if further assistance was required.

That kind of experience simply cannot be replicated online. If Amazon were to start selling Prada clothing anytime soon, the dissonance would be powerful. So while the luxury industry, and many in the retail sector at large, struggle with the idea of the shopper journey online, moreover how and where that connects with the physical journey, we cannot forget basics. The importance of good training, especially for demanding customer who are expecting a premium experience, cannot be overstated. Though smartphones and tablets may hold the data, it must be remembered that the purchase of a luxury product is often an irrational experience. The service and assistance received during purchase consideration may be an irrational influence, but it is an immensely powerful one. If a brand talks the talk, it must walk the walk, or face the consequences of failing to live up to its own promises.